Long-Term Care Insurance

Regardless of age, this is for you

I frequently receive this question, and the answer isn’t as simple as it may seem. Many people wait until it’s too late to purchase LTC and some purchase after they have had a personal experience with a family member who required care. However, the sooner you decide that long term care planning is right for you, the more options you have and the more affordable the coverage.

Long-term care insurance products are age-related and health underwritten. This means you can only get a policy if you are healthy and the younger you are, the lower the premium. If you were to develop a serious health condition between now and then, no amount of money will buy a policy. I got my policy at age 46 and now at age 61, I would not qualify. Better to buy now while you are insurable. I often get calls from people in their late 60’s and 70’s and it’s too late. They either don’t qualify or the payment is too high. They can’t do a life policy with a LTC Rider either.

No one plans to need long-term care. But the best time to buy protection is before that day ever comes. A person turning age 65 today has almost a 70% chance of needing some type of care in his or her remaining years. It often falls to the family and it is the hardest job in the world. Ask any caregiver what it was like. Many people have called me because they had to care for a loved one and said they would never put that burden on their kids.

Isn’t Long Long-Term Care for when I get OLD?

A fact of life: Someday you may need long-term care…and it may be sooner than you think. It might seem surprising that 40% of those receiving long-term care are under age 65! I know of young guy in his early 30’s and he had ATV accident who fortunately had a LTC policy. His policy activated, relieving his parents of a significant burden. When individuals have a serious, continuing health problem or disability, they frequently require long-term care. The need can come on suddenly like a disabling accident or in the case of a heart attack, stroke or chronic disease. Even dementia. However, it is most frequently caused by age, illness, or disability progression.

How does Long-Term Care work?

To be eligible for benefits, you’ll need a plan of care from a health care professional stating (1) that you require substantial supervision because you have a severe cognitive impairment, or (2) that you are unable to perform at least two Activities of Daily Living for at least 90 days. Activities of Daily Living are eating, bathing, dressing, toileting, transferring (to or from a bed or a chair), and caring for incontinence.

You’ll pay the cost of care yourself for the first few months. (That’s called the elimination period, and it can vary by policy – usually it’s 30-90 days. Most policies require you to satisfy the elimination period only once.) After that, long-term care insurance will reimburse you for covered costs.

Long-term care insurance has a daily or monthly limit on how much it will pay for reimbursable expenses, plus a lifetime limit on total payouts.

Long-Term Care Insurance vs other types of Insurance

People often confuse long-term care insurance with regular health insurance and disability insurance even though these types of insurance policies are vastly different.

Health insurance-

Regular health insurance covers medical care, helping to pay for medical bills resulting from sickness and injuries as well as physician and hospital visits. It does not pay for long-term care in most instances. In contrast, long-term care insurance is more about maintenance, assisting beneficiaries with the support costs for daily activities.

Long-Term Disability–

Long-term disability insurance pays for lost income, replacing a portion of income forfeited because you are unable to work as a result of an injury or sickness.

Medicare-

Medicare does not provide a benefit for long-term custodial care or care for chronic conditions. It is available to seniors and those who have disabilities, provides limited benefits for nursing home stays, paying only for acute, temporary conditions immediately following hospitalization. If your disability is chronic rather than acute, long-term services are not covered under Medicare.

Medi-Cal aka Medicaid–

Medicaid does provide assistance for long-term care needs, but only for those who meet strict income and asset limits. Eligibility for Medi-Cal varies by state, and for example, an individual would need to earn less than $18,754 per year in a state with expanded Medicaid.

In order to qualify for Medicaid’s long-term care benefits, you may need to liquidate your assets to meet your state’s requirements. You may also need to pay for a portion of your long-term care out of pocket and use the Medi-Cal spend down program which is designed for “medically needy”

What other options are there to pay for care?

Since regular health insurance plans, or disability coverage or Medicare doesn’t pay for long term care, here are your options-

1. Traditional Long-Term Care policy

These traditional LTC policies work much like policies for auto or home insurance: You pay premiums, usually for as long as the policy is in effect, and make claims if you ever need the covered services. Because the premiums are ongoing, they can, with the permission of state regulators, rise over time. But if you stop paying the premiums before the need arises, you usually lose the coverage. And if you never use the coverage, the insurance company keeps and invests your money to pay for other people’s claims and earn profits. It’s use it or lose it. You pay on your home insurance even though the odds of your house burning down are extremely small. With LTC, the odds are 70% once you attain age 65. So why not insure one of your greatest costs? If this is still not your cup of tea, then see the next option.

2. Hybrid Policy

The majority of long-term care policies sold since 2010 combine coverage for long-term care with another benefit, usually life insurance or, less often, an annuity, according to the Congressional Research Service. These are known as hybrid or linked-benefit policies. .

While in some cases, you’ll pay an ongoing monthly premium for such policies, many work like this: You pay one lump sum or a fixed amount broken into several annual payments, eliminating the risk of rising premiums. In return, you get long-term care coverage, along with some amount of life insurance that will go to your heirs if you never use the long-term care benefits. The life insurance payout is reduced or eliminated if you do use long-term care benefits. The policy may also allow you to take back your full payment within the first few years if you decide you no longer want the coverage.

The hybrid policies “address a nagging concern for a lot of people, … which is that I could pay into this thing for years and never need it. One way or another, you get a benefit. But that guarantee costs you. Hybrid policies are more expensive than traditional.

3. Family

Sometimes, I find it concerning when people express reliance on their children or spouse for care in their later years. Have they actually discussed this with their family? How feasible is it for a spouse to manage physical tasks if the individual requires lifting or assistance to move around? What if their children live far away? It’s unrealistic to expect a caregiver to balance a full-time job with providing consistent care. Would their child be willing to give up their career to provide care?

Personally, I wouldn’t want to burden my daughters or my wife with tasks like bathing or dressing me. Having witnessed the challenges of caring for my father during his final months, where his size and mental state posed significant hurdles, I understand the strain it can place on loved ones. In the end, we had to seek outside help because it became too much to handle alone. It’s crucial to consider the practicalities and realities of relying solely on family or limited care options like hospice.

4. Savings

Some people will look at their assets and spending and decide they can cover long-term care without insurance. Some may plan to sell a second home, downsize from a family residence or get a reverse mortgage (this is a rip-off) to cover such expenses. Others may set up a longevity fund to cover not only long-term care but also all the costs that come from living longer than average. One advantage of self-funding: total flexibility in how you spend your care dollars.

Even if you are very affluent, worth millions, your annual cost will be much higher because of the quality of care you will want. If you will use your savings, I am sure you will have it invested in the market. What if the market dips or crashes and then you need care so you take it then. That’s money you won’t get back if the market goes back up. Certainly you would have some set aside in cash or a CD, so why not leverage that?

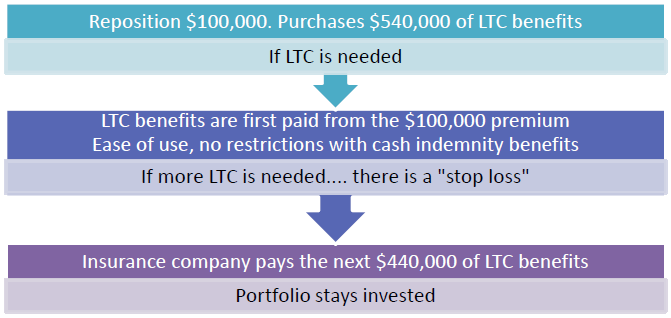

Cash Indemnity Policy

For example, lets say a person purchased a cash indemnity policy with no restrictions on how LTC benefits can be used will produce a different outcome. This same person places $100,000 into such a policy purchasing a LTC benefit pool of $540,000. Upon needing care, the first $100,000 of benefits would essentially be coming from their own premium dollars. But once that $100,000 is used up, the policy offers $440,000 in additional benefits available to pay for LTC expenses. And since the policy pays benefits by cash indemnity, the individual will maintain flexibility and control of care choices. By self-assuring, a “stop loss” is created for $440,000, whereas the self- insure plan would have no such insurance protection.

Think in terms of “SELF-ASSURE” instead of “self-insure”. At an average cost of care of $90,000-100,000 per year, let me show you a more effective way than using your retirement or savings.

Top Reasons of NOT getting a Long-Term Care Policy-

Here are the top 6 reasons people don’t get a LTC policy

1.I’ll pay for it all these years and might not use it.

I don’t want to pay for something I might not need is something I will hear often. That concern becomes a non-issue with Hybrid or Asset-based LTC products, which are guaranteed to provide ether a long-term care benefit while the policyholder is alive or a death benefit that passes to beneficiaries tax-free if the policyholder never uses the LTC benefit. I also think, well, I pay for fire insurance all these years and the odds of my house burning down are very low…I insure that asset so why not insure my savings with a policy.

2. I’m concerned the insurance company will raise my rates.

Historically, this has been an issue with traditional long-term care insurance. This is rendered moot by Hybrid or Asset-based LTC products, many of which can be purchased with a single premium. Or Hybrid products have an annual premium that is guaranteed never to increase.

3. With my health, I will not be approved.

With asset-based LTC policies, many cases are underwritten with a client phone interview and no medical exams. Also, Hybrid policies are have more lenient underwriting than Traditional LTC policies.

4. I don’t want another insurance policy. I want an asset on my balance sheet that has the potential to grow over time.

Because asset-based products are built on a life insurance or annuity chassis, their account or cash value may grow over time. Thus the value inside the contract is an asset that remains available to the client, and can be passed to beneficiaries if not used for LTC needs. In the case of life insurance, the proceeds can even pass income tax-free. “You’re getting an asset in an insurance product that serves the dual purposes of life insurance and protection from a long-term care event,” said Dennis Martin, FSA, FCIA, MAAA, Vice President, Senior Business & Product Development Officer, OneAmerica companies.

5. I’m concerned I’ll have to pay taxes on the money I withdraw from a policy to cover the cost of a long-term care event.

Withdrawals from asset-based LTC products for qualifying long-term care expenses are income tax-free if the contract is funded with after-tax dollars.

6. I want to see what the State of California is going to do.

California is talking about requiring everyone to get a LTC policy or pay a penalty The details will not be as robust as a traditional policy and there is there is little information of the costs and types of benefits and details. They are currently looking into the details and feasibility. They are also proposing a 1% payroll tax hike to help pay for this. Too much is unknown. I have heard that those who have a long term care policy will be exempt from any tax penalty. You can read more HERE.

Add Comment